Compliance Assurance

Discover how we uphold accountability & empower your financial journey with integrity.

Why Come To Ladder7?

Our Milestones Over The Years

1000+

Successful Plans Delivered

20+

Years Of Established Existence

300+

Happy & Active Client Base

15+

Countries, Trusted By Global Clients

60,000+

Hours Of Personalized Consultation Delivered

ladder 7

ladder 7

ladder 7

ladder 7

ladder 7

ladder 7

How We Made A Difference In Our Client's Lives...

True to their name, Ladder7 is helping us to scale success

We are delighted to share our positive experience with Ladder7 financial planning and wealth advisory firm. Their expert guidance and personalized approach empowered us to invest our money with confidence. The planner took the time to understand our financial goals and tailored a comprehensive strategy that aligned perfectly with our needs.

Throughout our interactions, they demonstrated a deep knowledge of the investment landscape and patiently addressed all our queries with utmost clarity. Their professional attitude and attention to detail gave us the assurance and peace of mind we needed to navigate the complexities of wealth management.

What truly stood out was their commitment to proactive communication and transparency. We were kept informed at every step of the journey, and their proactive updates and performance reviews reassured us that our investments were in capable hands.

Thanks to Ladder7, we now feel more secure about our financial future and have a clear roadmap towards achieving our long-term financial objectives. We highly recommend their services to anyone seeking reliable and trustworthy guidance in managing their wealth.

We recommend Ladder7 to anyone whos confused, over-confident and everything in between

We have been repeat customers at Ladder7. Despite being in the advisory business, Mr Suresh has managed to institutionalise certain values and practices that the younger team members ably represent thereby ensuring continued confidence from their clients. Its also reassuring when the team answers fundamental questions from a wide range of subjects from health insurance to real estate to bitcoins to ETFs to giving (charity) and much more. We recommend Ladder7 to anyone whos confused, over-confident and everything in between.

One of the standout qualities of Ladder 7 is their unwavering dedication to my financial well-being.

I have been associated with Ladder 7 since 2019. From the moment I engaged their services, I have known I am in capable hands. Their knowledge, expertise, and dedication to helping me achieve my financial goals have been truly remarkable.

First and foremost, Ladder 7 took the time to understand my financial situation, goals, and aspirations and created a comprehensive financial plan for me. Ladder 7 helped me identify areas where I could optimize my savings, minimize unnecessary expenses, and strategically allocate my resources. Their insights and recommendations are invaluable in maximizing my financial potential.

One of the standout qualities of Ladder 7 is their unwavering dedication to my financial well-being. Their proactive approach ensured that my investments are regularly reviewed and adjusted to align with my evolving objectives.Ladder7 team patiently listens to my all concerns and provides personalized advice tailored to my needs. Whenever I have questions or need guidance, Ladder 7 team is prompt in their responses and always provides clear explanations. Their ability to simplify complex financial concepts and present them in a user-friendly manner is greatly appreciated.One of the standout qualities of Ladder 7 is their unwavering dedication to my financial well-being.

I have been associated with Ladder 7 since 2019. From the moment I engaged their services, I have known I am in capable hands. Their knowledge, expertise, and dedication to helping me achieve my financial goals have been truly remarkable.

First and foremost, Ladder 7 took the time to understand my financial situation, goals, and aspirations and created a comprehensive financial plan for me. Ladder 7 helped me identify areas where I could optimize my savings, minimize unnecessary expenses, and strategically allocate my resources. Their insights and recommendations are invaluable in maximizing my financial potential.

One of the standout qualities of Ladder 7 is their unwavering dedication to my financial well-being. Their proactive approach ensured that my investments are regularly reviewed and adjusted to align with my evolving objectives.

Ladder7 team patiently listens to my all concerns and provides personalized advice tailored to my needs. Whenever I have questions or need guidance, Ladder 7 team is prompt in their responses and always provides clear explanations. Their ability to simplify complex financial concepts and present them in a user-friendly manner is greatly appreciated.

I wish everyone at Ladder 7 to keep doing the good works and JUST KEEP GROWING.

Sometime during COVID period, when everyone was scared, I just happened to look into my personal financial condition and was shocked to see how haphazard it was. I decided to take help of a fully fledged personal finance planner. Previously I had read articles published by Ladder & on different forums and I decided to call them. The first meeting was eventful and it made me at peace and thats when I decided to continue with them. They collected information with regular online meet and often on phone calls and e-mails. They helped me in every possible way and gave me details of my current condition and future financial road map. The simplicity, modesty and sincerity of the team were evident on their detailed discussions and calculations.

It has been 3 (three) years with them. I got to understand about different aspects of financial needs and the ways to meet up. I got understand about risks and their managements. Slowly but steadily my portfolio is being build and am very happy and pleased. It truly enjoyable and often I think what if I was engaged with them a few years before.People working there are safe, reliable and trustworthy. They are highly knowledgeable and always keep updating and also help us to enhance our knowledge by providing infobites and different articles.

Mr Suresh is quiet simple and a real gentleman. His book on IF GOD WAS YOUR FINANCIAL PLANNER is a must read for everyone. I must thank to Mr. Prateek, Mr. Shankar and Mr.Rohit for their enormous help and support. They are part of my family too. They are really prompt, precise and definitive.

I wish everyone at Ladder 7 to keep doing the good works and JUST KEEP GROWING. They are providing true fiduciary and ethical services in a client centric manner. I have no hesitation in recommending them.

The greatest factor in believing that I had made the right decision in having Ladder7 as my Financial Advisors.

I have been associated with Ladder7 for closely 2years. They came highly recommended through a very senior corporate leader and close friend.

What I really appreciated is their approach starting with a meeting in person along with Mr. Sadagopan. It gave the feeling of reassurance and the interest being taken to invent in their clients.

The meeting included a very candid conversation that covered career, family, financials and most importantly future financial commitments, career aspirations, potential life changes which could impact on many fronts. Having this conversation, which was open and yet not intrusive, gave a feeling of building a trust-based relationship. I believe the relationship with a financial advisor is like that with a doctor, whom you trust with your wellbeing and that of your family.For someone, who I have to admit, is terrible at managing finances, I found this a welcomed partnership. Some of the conversations were really tough ones which were required for me to understand how these things will impact me in the long run. As they say, some were surgical changes while some were not too drastic.

One of the main things I truly value in this client relationship with Ladder7 is that they have always advised me based on what is in my benefit and not with the idea to add to their business. They have also dissuaded me from taking on any financial commitment which may not have been in my best long term interest however could have been in their benefit and that for me was the greatest factor in believing that I had made the right decision in having Ladder7 as my Financial Advisors.

Each of their advisors have invested in understanding me as a client and what works best for my long term goals. In particular I would like to thank Rohit, Prateek and Shankar, for their patience on spending considerable amounts of time ensuring I have understood the nuances of investments, answering multiple queries and always being available to help me clarify any doubts as well as other financial clarifications as and when the need has arised. They have supported me by connecting me to the right people who manage other aspects of finance, which they do not necessarily cover, thereby reducing my stress of vetting the right agents.

I look forward to a long standing professional relationship with Ladder7 as we continue to ensure it is a financial success for both.

01 Blogs

Uncover insightful strategies for financial security and growth with in-depth articles on planning and wealth management.

02 Podcasts

Unlock the secrets to financial freedom and prosperity with expert insights and strategic wealth planning.

Engage with dynamic video podcasts, in-depth discussions, and cozy fireside chats that bring clarity and actionable strategies to your financial journey.

03 Infobites

Elevate your financial understanding with bite-sized insights on planning, investing, and goal achievement.

.jpg)

04 Media Presence

Experience wealth planning like never before through interactive videos, infographics, and webinars packed with actionable advice.

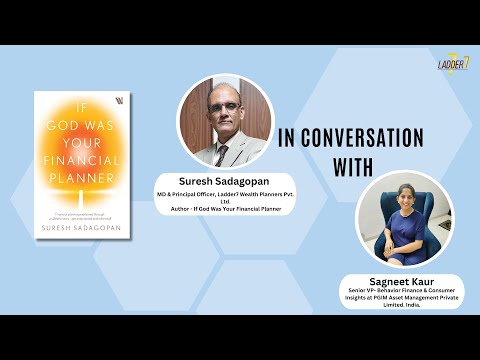

Factors To Consider When Investing For Children

Nidhi Sinha, K S Rao, Amit Trivedi & Suresh Sadagopan

Nidhi Sinha, K S Rao, Amit Trivedi & Suresh Sadagopan

Schedule a consultation today!

Our team of financial advisors will engage with you, understand your requirements and, advice on the way forward.

Let's Begin